If you don’t have a financial background and have recently joined a publicly listed company, or have recently been made responsible for a business unit or profit and loss center, then you’re going to need a quick guide to get you up to speed on some of the terms you’re likely to encounter.The higher you progress in your management career the more solid a grasp of financial terms and software you’re likely to require. Some of the terms listed below you may already be familiar with, but if you’re only familiar with less than half you may want to invest in some financial education.

I thought about various ways to organize the numerous terms described below, such as those applicable to start-ups, those applicable to larger organizations, and those everyone in business should know. But after experimenting with that a while, it made more sense just to list them in what I thought was the most sensible order. So, in order, the terms we’re going to cover are:

- Profit & Loss (P&L)

- Balance Sheet

- Income Statement

- Cash Flow Statement

- Contribution Margin

- Expense Allocation

- Return on Investment (ROI)

- Cost of Capital

- Net Present Value (NPV)

- Internal Rate of Return (IRR)

- Free Cash Flow

- Real Options Analysis/Theory

- Seed Money

- Stock Options

- Dilution

- Antidilution

- Share Buybacks

- Warrants

- Earn-Up and Earn-Out

- Price/Earnings Ratio (P/E Ratio)

- Carve Out and Spin Off

- Public Debt

- Debt Ratings

- Depreciation

- Amortization

- Impairment

- Goodwill / Intangible Assets

- EBITDA

- Return on Equity (ROE)

- Book Value

- Earnings Per Share (EPS)

- Market Capitalization

- Dividends

- Burn Rate

1. Profit & Loss (P&L)

Organizations may have individual profit and loss centres for business units, business lines, or even important products. To have P&L Responsibility means that you have responsibility for both the revenue and costs of your particular business unit.

2. Balance Sheet

This provides a financial snapshot of the company. The balance sheet shows the assets the company owns, such as property, automobiles, equipment, cash in the bank etc. It also shows the liabilities the company owes, such as accounts payable and loans owed to others. Shareholder Equity is a term you will come across if you investigate balance sheets, and is simply the amount of assets the shareholders own. It is calculated as assets minus liabilities. You might be wondering why its called a balance sheets – well it’s because it must balance as follows: Assets = liabilities + shareholder equity.

3. Income Statement

Also called the Profit and Loss (P&L) Statement shows the operating performance of the company. A P&L Statement will show you very quickly whether the company has made a profit or a loss during the year. It shows how revenues turn into the company’s net profit – how revenues come into the company, then have expenses against them, to end up with the company’s net income.

4. Cash Flow Statement

You might be wondering why a Cash Flow Statement is needed when the balance sheet shows the company’s assets, and the P&L Statement shows how the company made a profit or loss? Well it’s needed because the P&L Statement doesn’t necessarily show the true state of the company. For example, if a company sold a database for $1 million, but gave the company buying it 18 months to pay for it, then the company may have reported $1 million in earnings on the income statement but it has yet to receive any hard cash. If the company buying the database went bankrupt then it may never receive this $1 million. The cash flow statement shows the true financial performance of the company over the year by showing how real cash flowed into and out of the company’s bank account over the year, regardless of what has been reported on the income statement.

5. Contribution Margin

This is the incremental profit that each new product sale, or employee hired, or customer gained, generates. Knowing contribution margins allows you to understand key questions, such as how many employees you would need to take on to increase profits by 25%. Typically, high contribution margins exist in industries that are labour intensive, and low contribution margins exist in industries that are capital intensive.

6. Expense Allocation

This is where each operating unit (P&L Centre) must pay towards the organization’s general expenses. What this means will vary from company to company, but it typically includes debt, IT systems, human resources, legal, rent etc. A manager’s allocated expense allocation can seriously affect their ability to meet their P&L goals. Expense allocations can often explain why certain managers are strongly against new programs of work as it will increase their expense allocation. Because of this it is important to identify and then manage all stakeholders well by making the benefits of any such change clear to all.

7. Return on Investment (ROI)

On the surface this calculation is as simple as profits divided by the monies invested to generate those profits. However, in practice calculating either of the input figures can be complex. The problem with ROI is that it can be manipulated to suit the desires of the manipulator, for example, a financial analyst will calculate ROI in a very different way to a marketing executive.

8. Cost of Capital

In order for obtain a profit, any investment the company makes must be greater than the cost of the capital used to make the investment. If you’ve borrowed money to make the investment then the cost of capital equals the capital borrowed plus total interest repayable. If you don’t have to borrow then the cost of capital equals the capital plus the interest you could make on it risk free by investing in government bonds. You will sometimes see cost of capital referred to as the “hurdle rate” – the return you need to break even.

9. Net Present Value (NPV)

This is based on the time value of money. Net Present Value helps you understand the present value of an investment when the income from the investment is expected to arrive as a series of cash inflows in the future. For example, if a $1,000 investment generated $1,100 per year for 10 years ($11,000 in total) would the investment be worth it? No is the answer, because even modest inflation means that those future returns aren’t nearly as valuable as they are today.

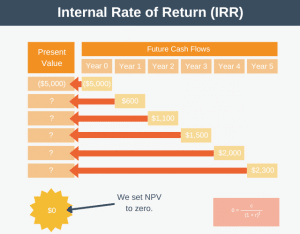

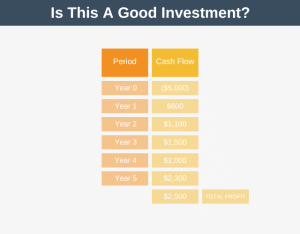

10. Internal Rate of Return (IRR)

You will often see this term called the discounted cash-flow rate of return, or sometimes just rate of return. Calculating IRR is one of the most popular ways of determining if a project is worth investing in, or not. This is similar to NPV, except that unlike NPV which provides a $ figure which can be difficult to interpret, IRR provides a % which many managers find more intuitive to work with. IRR is the return rate at which NPV equals zero. It also provides you with the project’s expected return rate. So in essence, the higher the IRR the more earnings the project will return.

11. Free Cash Flow

Provides another mechanism to measure the financial performance of a company. Free Cash Flow is the cash that an organization is able to generate, after spending any money needed to maintain or grow its assets. Because financial accounting tricks can sometimes obfuscate earnings calculations, free cash flow is a very good indicator of a business’ profitability, as it is very difficult to fiddle cash flows.

12. Real Options Analysis/Theory

This uses techniques developed to model financial options such as Black-Scholes Model, and adapts them to model real life decisions. Real Options Analysis can help you when you have to make difficult decisions like whether to invest in a new sales channel management system or whether to research a new product.

13. Seed Money

Sometimes called Angel Money, is money invested in an early stage company with the aim of getting it to an accretive milestone. An accretive milestone is simply a point at which the company can raise more money at a higher valuation. The monetary amount of seed money varies from company to company, but is usually less than $250,000. A typical mistake that entrepreneurs make is thinking that building the product itself is an accretive milestone. In fact, building the product is only an accretive milestone when there is a significant technological risk.

14. Stock Options

These are an extremely powerful tools for retaining talent. If the share price of the company rises, the employee will receive a financial benefit should they sell their stock. They are subject to a vesting schedule, which is a timeline specifying the minimum timeline upon which an employee can sell their shares. The shares will be allocated to the employee at a fixed strike price, usually the price of the shares when they are granted, and can be sold by the employee at an exercise price, usually the current market value at the point in time of sale.

15. Dilution

This happens when the company issues new shares to raise money and results in existing shareholders owning proportionately less of the company. For example, if a company has a total of 5 shareholders holding 1 share each, then the company is fully owned by those 5 shareholders. If the company now issues 1 further share to a new shareholder to raise capital, then the company is now divided between 6 shareholders. Note that each of the 6 shareholders would now additionally own ⅙ of the money paid by the sixth shareholder to purchase the additional share.

16. Anti-dilution

Anti-dilution is the opposite of dilution. An anti-dilution clause is used commonly by venture capital firms (VCs) to protect their shareholding – ensuring they hold proportionately the same percentage of stock even if the company’s stock is further diluted when raising additional capital.

17. Share Buybacks

A share buy back occurs when a company buys it’s own share at the current market price on the stock exchange. Essentially, share buy backs (when the shares are then cancelled as opposed to put in treasury) are a mechanism to provide capital gain to the company’s shareholders. When the company buys shares they reduce the total number of shares in circulation, thus boosting the proportional ownership of all the remaining shareholders. Note that sometimes the shares bought back by the company will be held in treasury, enabling the company to resell them or allocate them to employee stock option plans.

18. Warrants

These give the person or organization that holds them the option to purchase shares at a set price until a specific date, known as the expiry date. They are often used by cash strapped start-ups to help keep costs down. For example, rather than pay $50,000 in rent, a deal may be struck to pay the landlord $40,000 in rent and give them $10,000 in warrants. It will be no surprise to hear that this approach can often come back to bite the start-up if they become successful.

19. Earn-Up and Earn-Out

When one organization is acquired by another earn-ups and earn-outs give the founders (and key people) within the organization being acquired a reason to stay with the new organization and meet performance targets. They also benefit the acquiring organization. Earn-ups provide equity in the combined organization. Earn-outs provide cash.

20. Price/Earnings Ratio (P/E Ratio)

Sometimes referred to as earnings multiple, this is the measure of a company’s share price relative to its earnings (profits). It is used as an indicator as to whether a share is currently cheap or expensive. For example, a P/E Ratio of 10 indicates that a share is trading at 10 times its most recently reported earnings. P/E Ratios differ from company to company for a variety of reasons, but essentially a higher P/E ratio indicates that more earnings growth is expected from a company, whereas a low P/E ratio indicates that low or no growth is expected from a company. Essentially P/E Ratio is a market set interpretation about a company’s future – how it is expected it’s profits will grow, how strong it’s competitive advantage is, the market it’s in, it’s future products, and everything else which may impact the future profits of the company.